Two new HRA plan types are available: Individual Coverage HRA (ICHRA) and Excepted Benefit HRA (EBHRA).

On June 13, 2019, the Treasury, Department of Licensing (DOL), and Department of Health and Human Services (HHS) released final HRA plan regulations (ICHRA and EBHRA) that are effective for plan years beginning on or after January 1, 2020.

These regulations create two new HRA plan types:

- Individual Coverage HRA (ICHRA)–can integrate with individual medical insurance (or Medicare)

- Excepted Benefit HRA (EBHRA)–not required to be integrated with other coverage

In this post, we provide detailed information about each of these new HRAs. You can also watch our webinar covering the differences, benefits, and best practices for all HRA plan types, including an in-depth look at the two new HRAs. In the webinar you will learn:

- When ICHRAs and EBHRAs are a good fit for employers

- What expenses are eligible under an ICHRA or EBHRA

- Requirements for ICHRAs and EBHRAs

- Comparison of ICHRAs vs. QSEHRAs

- Comparison of all HRA plan types (traditional group coverage HRA, QSEHRA, ICHRA, and EBHRA).

Watch the ICHRA Fundamentals webinar.

Download the full 2020 HRA webinar presentation.

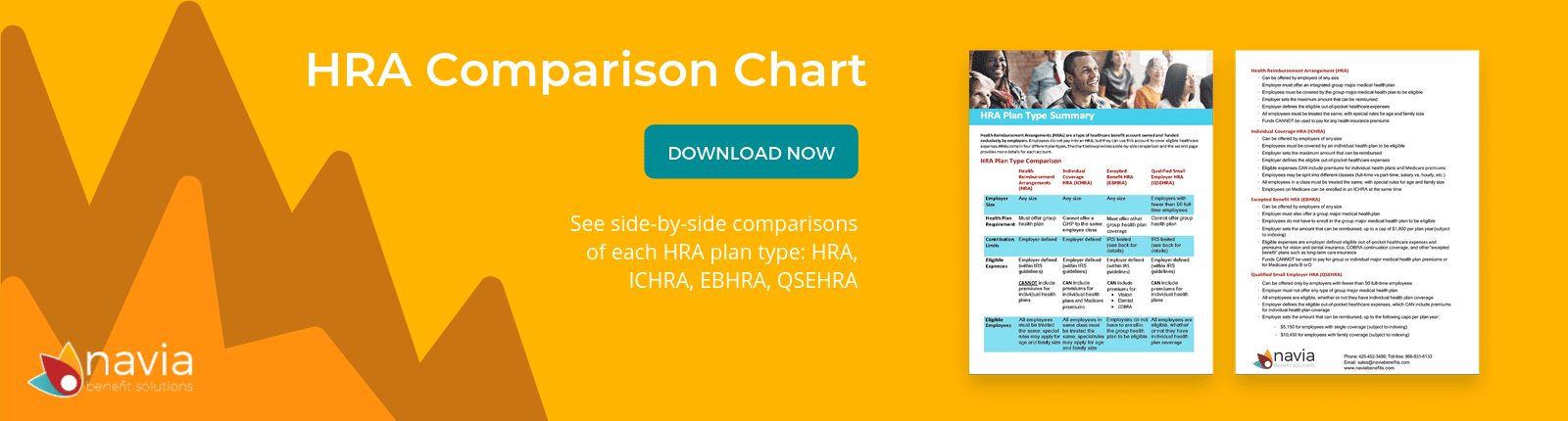

Download the HRA Plan Comparison Chart.

Individual Coverage HRA Plan (ICHRA)

Employers of any size can establish an HRA that reimburses the employee’s premiums for individual major medical insurance or Medicare, or other out-of-pocket health care expenses. Unlike QSEHRAs, ICHRAs are not subject to statutory limits on the benefit amount that can be provided. Also, ICHRAs will be available to Employers of all sizes (vs. a QSEHRA that is limited to small employers with less than 50 full-time employees). Employers can offer different amounts to different classes of employees:

- Full-time

- Part-time

- Seasonal

- Employees covered under a collective bargaining agreement

- Employees who have not satisfied a waiting period for coverage

- Employees who are paid on a salaried basis

- Non-salaried employees (e.g., hourly employees)

- Employees in different locations, based on geographic rating areas

- Employees who are in a combination of two or more of the classes (e.g. full-time employees covered by a particular collective bargaining agreement)

ICHRAs are subject to several requirements, outlined below.

Enrollment in Individual Medical Coverage (IMC)

The ICHRA is limited to employees and their dependents who are enrolled in individual health coverage or Medicare coverage for each month that they are covered by the ICHRA. Also, annual substantiations generally must be provided no later than the first day of the Plan Year.

No Traditional Group Health Plan (GHP) Offered to Same Employees

Employers cannot offer a “traditional” GHP to employees in the same class that is offered an ICHRA. However, an employer can offer such employees participation in a Health FSA or GHP that consists solely of excepted benefits (dental and vision). The regulations allow for defining employee classes on a common-law rather than controlled group basis. This allows an employer that is part of a controlled group to look at each individual employer when determining the classes of employees that will be offered either the traditional GHP or an ICHRA. If the employer offers both the ICHRA and a group health plan and chooses to structure the eligibility based on full-time or part-time status, salaried or hourly, or geographic location, they must ensure those groups receiving the ICHRA are of a certain size. The minimum-class-size is:

- 10 employees if the Employer has fewer than 100 employees

- A number (rounded down to a whole number) equal to 10% of the total number of employees for an Employer with 100 to 200 employees

- 20 employees for an Employer with more than 200 employees

Same Terms Apply to All Employees Within a Class

With three exceptions, employers that offer an ICHRA to a class of employees must offer it on the same terms and conditions to all employees in the same class (same maximum dollar amount and other terms and conditions). The three exceptions to this rule are:

- Age: Age based variations in an ICHRA cannot exceed the 3:1 ratio allowed for individual market premium differences based on age (the premium for the oldest person cannot exceed three times the premium of the youngest person).

- Number of Dependents: The maximum dollar amount available under an ICHRA may increase as the number of participant’s dependents covered under the ICHRA increases (on a uniform basis within the class).

- Former Employees: An ICHRA may be made available to some, but not all former employees within a class.

Right to Opt Out Annually

Employees who are eligible for coverage under an ICHRA must be permitted to opt out of and waive future reimbursements from the ICHRA (on behalf of themselves and all eligible dependents) with respect to each plan year. The ICHRA may establish timeframes for enrollment in (and opting out of) the HRA, but an opt-out opportunity must be provided in advance of the first day of the plan year.

For participants or dependents who become eligible midyear, or participants who become eligible fewer than 90 days prior to the plan year, this opportunity must be provided during the applicable ICHRA enrollment period. Upon termination of employment, ICHRA participants must either forfeit the remaining balance (subject to COBRA) or be permitted to permanently opt out of and waive future reimbursements on behalf of themselves and all covered dependents. This opt out provision is all about giving employees the ability to preserve premium tax credit eligibility.

Must Substantiate Enrollment in Individual Medical Coverage or Medicare Annually and Ongoing

The employer/plan sponsor must have reasonable procedures to verify enrollment in IMC or Medicare annually (before coverage begins) and ongoing (prior to each reimbursement). Annual substantiations generally must be provided no later than the first day of the plan year. The regulations offer two ways to substantiate enrollment:

- A document from a third party (e.g. the insurer or an Exchange) showing that the participant (and any dependents covered by the ICHRA) are, or will be, enrolled in IMC (e.g. an insurance card, EOB or documentation from the Exchange).

- The participant’s attestation, stating that the participant (and any dependents covered by the ICHRA) are, or will be, enrolled in IMC, the date coverage began or will begin and the name of the coverage provider.

Ongoing substantiations are required with each request for reimbursement, showing that the participant or dependent who incurred the expense for which reimbursement is sought continues to be enrolled in IMC for the month in which the expense was incurred. This may be in the form of the participant’s written attestation (which may be part of the reimbursement request form) or a document from a third party (e.g., the insurer) showing that the participant or dependent was enrolled in IMC for the applicable month. Note that the individual’s loss of eligibility to participate in the ICHRA due to the individual’s failure to maintain IMC (due to failure to make premium payments) does NOT create a right to COBRA under the ICHRA. However, the ICHRA must reimburse eligible expenses incurred before the individual’s termination of IMC (the ICHRA may establish a reasonable specified period for submitting these expenses).

Employer Written Annual Notice 90 days before ICHRA Plan Year

The employer/plan sponsor must provide written notice to participants at least 90 days before the start of the plan year (or no later than the date on which the participant is first eligible for newly eligible employees. The written notice must address:

- Terms of the HRA, including the maximum dollar amount available and any rules regarding the proration of the maximum dollar amount for participants or dependents who are not eligible to participate for the entire plan year.

- A statement that participants and any covered dependents must be enrolled in IMC or Medicare.

- A statement that the coverage cannot be short term limited duration insurance or consisting solely of excepted benefits (dental/vision insurance).

- The date when coverage under the ICHRA may first become effective.

- The dates on which the ICHRA’s plan year begins and ends.

- A statement of the right to opt out of and waive future reimbursements from the ICHRA.

- A description of the potential availability of the premium tax credit (PTC) if the participant opts out of and waives future reimbursements from the ICHRA and a statement that an offer of coverage will prohibit the participant (and potentially any dependents) from receiving the PTC on an Exchange.

- Employee’s obligation to inform any Exchange of the terms of the ICHRA.

- A statement of the participant’s responsibility to inform the employer if the participant or a dependent is no longer enrolled in qualifying IMC.

ICHRA Can Now be Purchased on a Pre-tax Basis

Employers can allow employees to use pre-tax cafeteria plan salary reductions to pay the portion of the premiums for their IMC not covered by the ICHRA, as long as the coverage is purchased outside of an Exchange. The requirements of Section 125 would apply to the plan, including having either a Premium Only Plan or amending existing Section 125 plan language allowing for the IMC pre-tax benefit.

Excepted Benefit HRA Plan (EBHRA) ICHRA

Employers of any size can also offer “limited-dollar” non-integrated HRAs that qualify as excepted benefits. These Excepted Benefit HRAs (EBHRAs) are also available for plan years beginning on or after January 1, 2020. This is a standalone HRA that an employer can offer to active employees who are eligible for a GHP (not necessarily enrolled, but eligible). EBHRAs are subject to several requirements, outlined below.

Employer Must Offer GHP to Same Group of Employees

The employer must make other GHP coverage available to the EBHRA participants for the plan year; however, enrollment in the other GHP is not required.

Limited Benefit Amount

Not more than $1,800 (indexed for cost-of-living changes after 2020) can be newly available to each participant for each plan year (carryovers are permitted and disregarded in terms of the limit).

Cannot Reimburse Certain Premiums

An EBHRA may reimburse out-of-pocket Section 213(d) medical expenses, but cannot reimburse premiums for IMC, Medicare or non-COBRA group coverage.

Uniform Availability

An EBHRA must be made available under the same terms and conditions to all similarly situated individuals. In addition, the employer cannot condition enrollment in the EBHRA on declining to enroll in the traditional GHP. Also, employers cannot offer both an ICHRA and EBHRA to the same class of employees.

There is no notice requirement for EBHRAs.

Download the full 2020 HRA webinar presentation.

Watch the webinar presentation now.

Download the HRA Plan Comparison Chart.